Abacus Global Management is Performing Beyond my Most Optimistic Expectations $ABX

I have been pounding the table on Abacus Global Management (ABX) since my first writeup in January of last year, but I was wrong about two things. I underestimated how well management would execute on their opportunity, and I overestimated how quickly the market would give them an appropriate multiple.

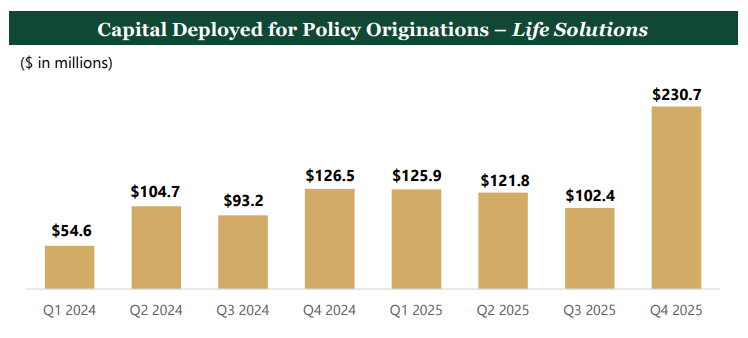

The current limitation on Abacus’ business is the speed at which they can originate life settlements. I have written in the past about the acquisitions which will allow Abacus to capture more value from each life settlement, but the real bottleneck is how much capital they can deploy. I was completely blown away by ABX deploying $230 million in Q4 2025. To put that growth rate in perspective, ABX deployed $219 million in all of 2023.

In Q4 of 2022, ABX deployed $35.5 million.

In Q4 of 2023, ABX deployed $68.3 million.

In Q4 of 2024, ABX deployed $126.5 million.

In Q4 of 2025, ABX deployed $230.7 million.

And even more importantly, CEO Jay Jackson regarding capital deployment said, “we expect this momentum to continue accelerating in 2026. Chief Capital Officer Elena Pasco, who is part of the team who will be buying life settlements from private credit funds, said, “As we enter 2026, our capital deployment pipeline is robust.”

I had expected the growth rate to slow somewhat. It isn’t reasonable to expect a company to nearly double the size of their business every year. And yet here we are, with ABX’s business nearly doubling every year for four years, ok, to be fair, compounding at an 86.61% cumulative growth rate.

For paying subscribers I’ll go into detail about what this amount of originations means for 2026 earnings:

Keep reading with a 7-day free trial

Subscribe to Value Degen’s Substack to keep reading this post and get 7 days of free access to the full post archives.