A Little Industrial Trading at 1x 2025 EBITDA: Alta Equipment Group (Reprise) $ALTG

It’s becoming harder and harder to find small cap companies that I like better than what’s already in the portfolio. At the same time, some of my newer subscribers weren’t around for some of the older names I’ve written about, and it never hurts to re-underwrite the thesis anyway.

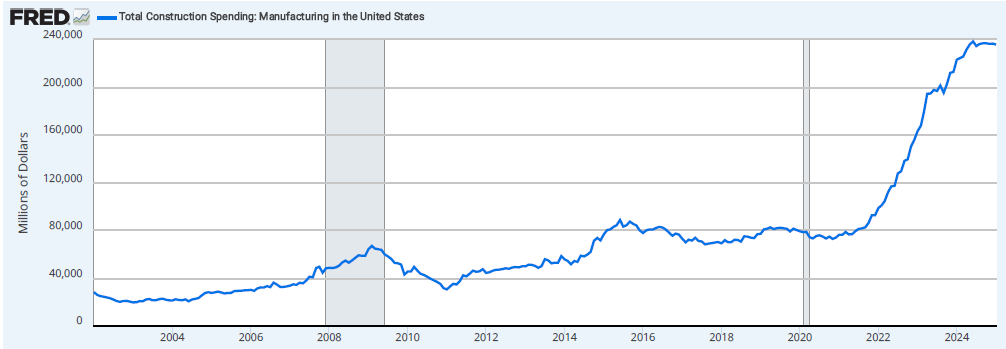

Alta Equipment Group (ALTG) has suffered under the hands of this recent selloff. The market capitalization has been compressed to $174 million, which coincidentally is the lower end of management’s 2025 EBITDA guidance of between $175 million and $190 million. There are decent odds that management is cautious with guidance due to Trump tariff uncertainty, but ALTG is a beneficiary of reshoring. I believe that annualized EBITDA from the twelve months including H2 2025 and H1 2026 will be over $200 million. Have you seen the chart of manufacturing construction spending since Covid?

Alta Equipment Group is a founder-led construction equipment and forklift dealership business rollup. The CEO, Chairman of the Board, and son of the founder owns about 17% of the company, and was engaging in insider purchases when the stock was trading above $14 per share.

The United States has a legacy monopoly system for dealership businesses dating back to the Great Depression. When manufacturing capacity was limited, Henry Ford and the other industrialists only supplied dealerships who were willing to sign multi-year purchase agreements. When the Great Depression came, the dealerships were unable to honor their purchasing commitments, and the courts at that time still honored contracts. The states were unwilling to let their influential local businessmen go out of business, and so they created monopoly licenses that persist to this day. By giving those valuable licenses to the dealers, the local businessmen were able to dig themselves out of the hole they had found themselves in. If you have the Ford dealership for a region, you have the only Ford dealership for that region. Tesla overcame this by opening their own showrooms and bypassing dealers all together.

Most importantly, if you have the only dealership in the region, you have a monopoly on parts and service. Unlike for automobiles where parts can be found easily at AutoZone or their competitors, construction machinery and forklifts are much more captive. ALTG’s primary forklift manufacturer, Hyster Yale (HY), has a rule in place that their dealerships are not allowed to be owned by a private equity group, which takes one of the biggest small cap investing risks off the table; there isn’t much risk of ALTG getting taken private while prices are suppressed. Also, to streamline their operations, Hyster Yale has been encouraging consolidation among their dealership groups so that they have fewer entities to engage with. The rollup wasn’t entirely Alta Equipment Group’s idea.

Alta Equipment Group has been rolling up these machinery dealerships, making 16 acquisitions since their IPO in 2020. Prices for acquisitions come in at around 4x to 5x EBITDA, although one dealer in particular was so eager to join ALTG that they sold for 3x EBITDA. All rollups claim that acquisitions are accretive, but ALTG’s acquisitions caused one of the rarest accounting line items, “gain on bargain purchase,” where something is worth more in book value than what was paid for it; it’s the opposite of goodwill, and good luck ever finding it again. There is still a lot of room to grow, Hyster Yale hasn’t reached their desired degree of dealership consolidation yet. ALTG hasn’t made an acquisition in two years, but they still have another $300 million undrawn on their revolver.

The dealership business model is a blend of the highly cyclical equipment sales and the counter cyclical parts and service revenue. With the exclusive monopoly for the region, every machine sold leads to a certain amount of parts and service revenue in the future, and old equipment needs to be maintained, even if new equipment sales are in a slump. From the chart below, you can see parts and service revenue growing, even as new equipment sales fell in 2024.

New equipment sales have been in a slump, as would be expected from rising interest rates. But due to the Covid supply chain crisis, there was a backlog of orders that dragged on into 2023 despite a massive slowdown in manufacturing. But 2024 was a trough year, there was no more Covid backlog, and the full effect of higher interest rates weighed on the market. Management has already guided that activity in Q4 2024 picked up dramatically after the election, although there is always a seasonal holiday slump for that quarter. And, uncertainty in Q1 2025 has been higher than many anticipated as Trump’s second administration differs in some ways from his first.

Manufacturing activity has been in a recession since October of 2022, with ISM Manufacturing coming in below 50 until this recent January and February data points. These last two months have had uncertainty surrounding tariff policy, and the 10-year treasury had crept up. But we are still in a global interest rate cutting cycle, and the tariff uncertainty is likely to be resolved in the first half of 2025. With Trump’s deregulation initiative, the potential for lower taxes, more accelerated depreciation, falling interest rates, and more of a reshoring emphasis, it is very likely that ALTG will return to growth in 2025, and with the second half better than the first half.

ISM Manufacturing Survey:

In the middle of 2024, ALTG refinanced their debt out to 2029, but at a 9% coupon. This added interest expense is burdensome, and it has completely canceled out the benefits of the economies of scale that ALTG achieved through the rollup. SG&A as a percent of revenue has fallen from 25% to 23% as a result of the rollup, adding about $40 million annually to the bottom line, which is now entirely eaten up by the interest expense. The current capital allocation priority of management is to pay down debt, and they did pay down $60 million in the last six months, but this was mostly due to a working capital release and not operating cash flow. ALTG does have about $15 million remaining on a share buyback program authorization, but for the most part, their priority for cash flow is to pay down debt.

ALTG has debt from two sources, not just the debt from the acquisitions, but dealerships use floorplan financing programs for their inventory. If interest rates were to spike significantly higher, that would pose a threat to Alta Equipment, because at the moment they do have significant leverage. Looking past the floor plan financing, long term debt to EBITDA is about 4.1x. This multiple is temporarily high due to compressed EBITDA in 2024 of $168 million compared to 2023’s $191 million, and 2025’s guidance of between $175 million and $190 million. It does look like ALTG’s recent poor performance really is temporary, as management’s guidance and the ISM manufacturing survey agree. But even at $190 million of EBITDA, the long term debt to EBITDA ratio is still 3.65x. It is a sign of a quality business that the ISM survey has been below 50 for the longest period ever, 26 consecutive months, and ALTG had over $30 million of free cash flow in 2024.

If the economy were to stumble from here, which I don’t believe is likely, but is always worth considering, management believes they can make it through with their parts and service revenues and $300 million undrawn on their credit facility. I believe it is much more likely that ALTG is entering a cyclical boom for their business, but I am basing price targets on more moderate scenarios.

Looking at valuations since IPO, they are remarkably stable at around 8.0x EBITDA to Enterprise Value. This means that the $23 million dropoff in EBITDA led to a loss of almost $200 million in market capitalization. The high levels of leverage leave only about $174 million left for the market cap. But every little bit of debt paydown goes a long way toward adding shareholder value. Based on management’s guidance of around $25 million of free cash flow for 2025, applying that toward the debt, and an 8.0x EBITDA / EV ratio gives a share price of $10.97 for the end of 2025, and $14.51 for the end of 2026. Not too bad for a company trading at $5.10. Those numbers could change if management leans into their share buyback program, or engages in any new acquisitions.

It also ignores the possibility of a boom in their particular business, which is highly likely given Trump’s accelerated depreciation programs and the reshoring impetus. The time to buy new forklifts and construction equipment is probably upon us. A boom year, which is very likely starting in the second half of 2025, could easily generate $100 million to $150 million of annualized free cash flow. Which would go a very long way toward paying down some of the $695 million of long term debt.

The monopolistic nature of the dealership business and the recurring parts and services revenue gives ALTG a claim to eventually becoming a quality stock. But in the meantime, I am treating this as more of a short term trade instead of a longer term investment. I am willing to change my mind if management is able to squeeze any efficiencies out of their system and generate enough free cash flow to pay down the debt rapidly, or refinance and engage in more acquisitions. A reduction of SG&A to 21% of sales would be another $40 million annual free cash flow to retire debt. And at these prices, even their modest $15 million authorized share buyback program would go a long way if utilized.

Alta Equipment Group (ALTG) $5.10: $10.97 by end of year 2025

Alta Equipment Group (ALTG) $5.10: $14.51 by end of year 2026

I went through their Annual report, but just don't see the capacity for paying back debt if the operations don't increase materially. All their operating cash flow went to Capex. Why they still pay dividends and do share repurchases is beyond me.