On September 29th, I wrote about Hooker Furnishings (HOFT):

Government Shutdown? Growth Scare? Hookers? Hooker Furnishings $HOFT

The S&P 500 is in the 99th percentile for the longest rallies without a 5% pullback. So many historical trends have been broken in these last few years, I don’t put much confidence in the idea that we must have a selloff. But a lot of market participants sound like Shaggy and Scooby slowly exploring a haunted mansion, and all it would take is for some m…

So imagine my surprise when I discovered a furniture company founded and still operated by the Virtue family. Virco Manufacturing (VIRC) is an educational furniture company founded by Julian Virtue in Los Angeles in 1950. Last week, his son and current CEO Robert Virtue as well as his grandson and current President Douglas Virtue engaged in a bit of insider buying.

The stock price of VIRC has been crushed for the last year. It was a somewhat famous microcap short thesis in 2024, based on the idea that VIRC had been temporarily over earning, but the margins would return to historical norms. Things might be turning around for VIRC now, they manufacture entirely within the US, and with the new reciprocal tariffs, it might be their time in the sun. The Virtues seem to think so, although insiders have notoriously bad timing, even if they are good at detecting undervaluation. Maybe the stock was a short at $18, but maybe it’s a buy at $7.40 with consensus 2026 earnings per share of $1.15.

The educational furniture market is a bit unique, typically 50% of revenues come during the back to school season in the fall. Long term growth for the domestic US educational furniture market still points to a 6% growth rate, but 2025 was relatively weak. Virco has grown revenue at a 4% annual rate for the last ten years, from $179 million in 2015 to $269 million in 2024. Educational furniture is highly cyclical, and is also tied to interest rates. When housing transactions are frequent, property taxes are set to the new sales price. When the housing market has been frozen, school budgets are under pressure. And of course, Covid was a particularly tough time.

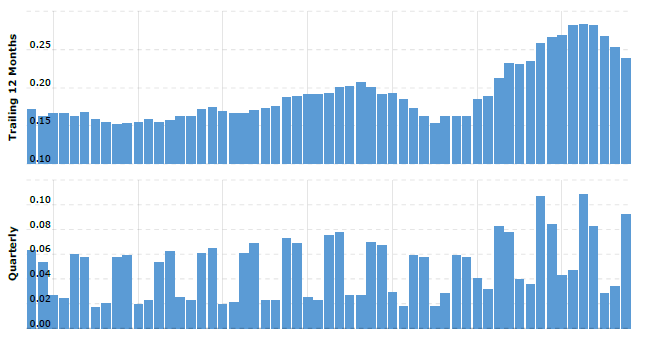

Virco Revenue:

While I don’t have the data from this current back to school season yet, going into this season the order backlog was down by 30% over last year. Still, the Virtue management team has been focusing on cost cutting, and even on lower volumes, Virco had its most profitable quarter in years. Virco probably has between 20% and 30% of the domestic educational furniture market, and there is a chance to take market share due to the reshoring emphasis. Many of their competitors also manufacture in the US, but three out of seven are importers.

Furniture is a terrible business, but even a terrible business can double in price due to cyclicality and share buybacks. Virco had not instituted any return of capital to shareholders since being founded in 1950 until the post Covid slump in 2023. Starting in 2023, Virco initiated a humble dividend of $0.02 per quarter, and a share buyback program of $5 million, retiring 1.7% of the float. In January of this year, another $10 million was authorized under the share buyback program, and if fully deployed, would retire between 5% and 8% of the float due to the current lower share price. With various members of the Virtue family owning a combined 34% of Virco, I wouldn’t be surprised if the share buybacks continued until the price rebounded, or until the family could take it private with a modest bit of leverage. With $33 million of operating cash flow in 2024, and a $116 million market capitalization, if Robert and Doug get frustrated with the share price, those shares will get gobbled up.

Virco initiated cost cutting and efficiency initiatives post Covid. Since those efficiency initiatives, they have enjoyed GAAP net income of $16.5 million in 2023, $21.9 million in 2024, and $21.6 million in 2025. Before this transformation, the average net income for the ten years prior was $550,000. This is a company who was once a fiefdom meant to give some clout to the founding family by having as many employees to lord over as possible. But now it’s a cashflowing share gobbler trading at a trailing price to earnings of 5.3x with decent odds of heading into a secular boom within the next two years.

It looks like the stock price may have found a floor, or it may continue to be a falling knife until we have more evidence of the secular tailwinds. The combination of revenue growth, share buybacks, and cyclicality make Virco a likely double, returning to a share price of around $15 from the current $7.40. But I wouldn’t personally buy more than a placeholder position before the next quarterly earnings call. With the order backlog down 30%, this back to school season is likely to disappoint. But I do think there are good odds that the stock will find its floor before Trump appoints his new Fed chair in May. In a world where so many things feel expensive, a family operated, 75 year old domestic manufacturing company buying back shares aggressively and with room to double is refreshing.

Virco Manufacturing (VIRC) $7.40: $15 at the next cyclical peak within two years