A Better Ensign than Chekov?: Ensign Energy Services $ESI.TO

Note: I will be away at a conference for the next three days, so there won’t be a new writeup for Thursday and Friday of this week. Best regards! - UVD

I was watching a recent interview with

of Bison Interests, and for the first time in a long time, he dropped a small cap stock idea for us to dive into. Josh hasn’t tossed a breadcrumb for a while, possibly because the entire energy sector has been dead for two years, and possibly because one of his previous darlings, Journey Energy, has a CEO who has been acting as though he might be having a psychotic break. But I’m not throwing stones, I did my own due diligence in Journey, and I found the CEO to be scrappy and with aligned incentives, I bought a bit, the stock price fell, and I sold at a loss. Nobody’s fault but mine.Now Josh has a new idea, and it’s in my favorite slice of the energy pie, oilfield services. But unlike my darling ProFrac Holdings (ACDC), he prefers onshore drilling rigs over frac fleets. His reason? The life of the asset, drilling rigs last many more years than frac fleets, and this leads frac fleet companies to have much larger maintenance capex. This is a bit of a double-edged sword, the frac fleets, with faster depreciation, will reach their cyclical inflection much faster as equipment is retired earlier. But in the meantime, the drilling rig operators have a much greater pass through from operating income to cash flow.

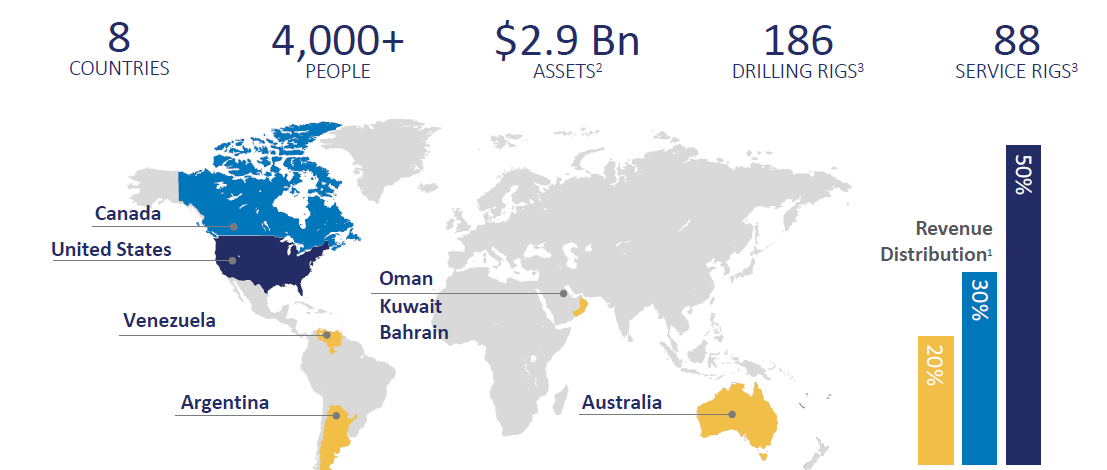

So without further ado, I present to you, something borrowed but not blue, Ensign Energy Services (ESI.TO), a Canadian oilfield services company with a focus on drilling rigs. But to call them Canadian is short shrift, only about 30% of revenues come from Canada, 50% comes from the US, and the remaining 20% comes from Argentina, Venezuela, Australia, Oman, Kuwait, and Bahrain.

While their business is diversified, their debt is about 50/50 CAD/USD denominated. I find Canadian debt to be some of the best in the world at the moment, because the game theory of the Canadian housing market tells me that they will need to depreciate their currency no matter who wins in the next election. So Ensign will have the ability to earn US dollars, and to repay debt in Canadian pesos.

How much debt does Ensign have? About 1.55 billion CAD in liabilities compared to 2.88 billion CAD in assets, 53% debt/equity. Trailing twelve month EBITDA is 475 million CAD compared to interest expense of 105 million CAD, 22% interest/EBITDA. That compares to ProFrac (ACDC) with $3.13 billion in assets and $1.96 billion in liabilities, a 62% debt to equity ratio. And $357 million in EBITDA to cover $156 million of interest expense, a 43% interest/ EBITDA.

Given that Ensign has the better balance sheet, one might expect that it would have a higher valuation, but one would be wrong. ACDC trades at 0.57x price to sales to Ensign’s 0.33x. And ACDC trades at 1.15x price to tangible book compared to Ensign’s 0.42x. ACDC is about twice as expensive as Ensign, which leads me to believe that Ensign is misunderstood and is being priced as a Canadian company despite the international diversification.

Regarding governance, ACDC has the Wilks cousins, guided by their fathers, the Wilks brothers, who in their generation built and sold an oilfield services company. It’s a great blend of youthful energy with experience and relationships. But Ensign is 26% owned by Murray Edwards, the Executive Chairman of Canadian Natural Resources (CNQ), the $65 billion market capitalization best-in-class Canadian energy company. So Ensign has incentive alignment, experience, and relationships as well.

Is Josh Young correct, are oil rigs a better business than frac fleets? Well, Ensign has 475 million CAD EBITDA from 1.688 billion CAD of revenue, a 28% EBITDA margin. ACDC has $357 million EBTIDA from $2.225 billion revenue, a 16% EBITDA margin. Although to be fair, ACDC has their sand mines and manufacturing business, both thin margin, and at least one destined to be spun off. So the margin comparison is not pure.

But even without a pure comparison, Ensign is cheaper, more profitable, internationally diversified, and competently led by the best energy executive in Canada. There is also insider buying from Ensign’s COO, CFO, and one of their directors as well. I’m convinced, sign me up, I am happy to buy some ESI.TO.

The debt maturity situation is a bit ugly, most of the debt is on a rapidly amortizing three year revolving facility. But refinancing has been at tolerable interest rates, and the EBITDA is just about large enough to pay off the amortization schedule. I would predict that Ensign will refinance a portion of that debt, it doesn’t make sense to spend the next three years becoming debt free when the Canadian central bank is cutting aggressively.

The thing about a fund manager pumping a stock is that he has already acquired his full position. And with that buying pressure suddenly stopping, oftentimes this can cause the stock price to fall, even if he isn’t selling into the pump. But Ensign’s stock price hasn’t moved up too significantly recently, it was at 3.50 CAD in September of 2023, but subsequently fell to 2.12 CAD in June of 2024. Since that June low, Ensign’s stock price has rallied to 3.05 CAD, but at their current multiples, can hardly be called expensive or overdone.

The larger oilfield services companies trade at a price to tangible book of over 2.5x. Even if that high multiple is out of reach for Ensign, it could probably trade back to a 1.5x price to tangible book ratio, and that tangible book value is growing with debt repayment. Assuming a tangible book value of 1.5 billion CAD by the end of 2026, and a 1.5x price to tangible book multiple, that would be a 12.43 CAD stock price by the end of 2026. I think the market might need another year to value Ensign fully, so for a margin of safety, I’ll say 2027 instead.

Ensign Energy Services (ESI.TO) 3.05 CAD: 12.43 CAD by end of year 2027

I've been buying ESI recently as well. I even have a write-up queued for next week.

Though it's nice to see the debt levels trend down since their peak from the Trinidad acquisition, they are still high. That does give it a bit of de-leveraging upside I suppose.

I like that Edwards and Fairfax having such large positions.