2024 Q3 Earnings Update Part IV: Medical Properties Trust $MPW, FTC Solar $FTCI, Nerdy $NRDY, Portillo’s $PTLO and Opendoor $OPEN

Hello and Welcome to Part IV of the Q3 Earnings Call updates. The market these days is at a bit of a crossroads. Nvidia (NVDA) reports earnings on Wednesday, I believe, and it’s possible that the market is looking to this earnings report to decide whether the Artificial Intelligence narrative will be strong in 2025. If AI is going to be weak in 2025, then a lot of fund managers would sell in January to rotate to other sectors, and of course, if everyone knows everyone will rotate sectors in January, then fund managers would want to get in front of that and rotate sectors immediately. So I might not be paranoid to think that Wednesday’s NVDA earnings report will set the tune that market dances to for 2025. We will see.

I sat down with Mitch over the weekend to look at some technical analysis. This is the sort of thing I should make sure to share on Monday, but I have been preoccupied with crypto recently. The combination of fundamental and technical remains a huge priority for me, as I have taken a few too many lumps relying on fundamental analysis alone in the past. Even I don’t want to catch every falling knife anymore.

Medical Properties Trust (MPW)

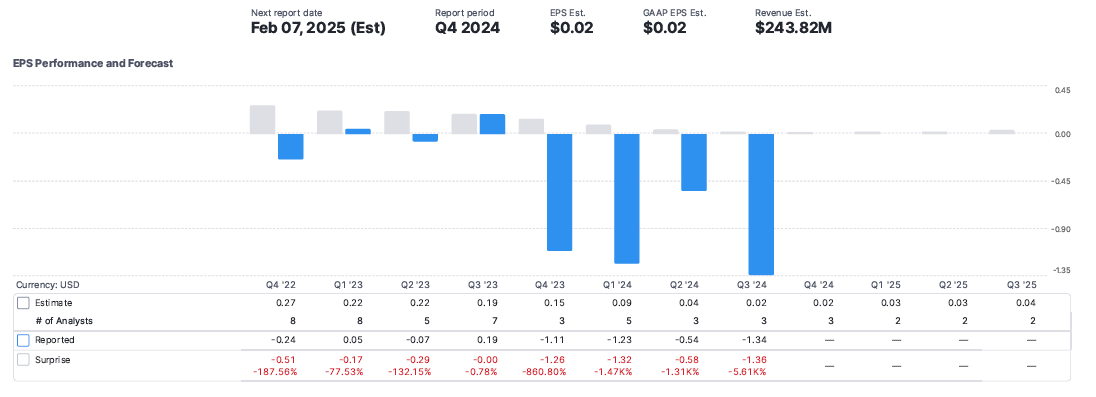

I have to admit, the recent price action of this stock has been a source of pain. I would not have predicted the stock price to stay suppressed despite both tenant problems coming to resolution: Prospect successfully selling their managed care business and the Steward bankruptcy process resolving. But, I am learning that the majority of money in the marketplace is quantitative, and that money will stay short MPW until their earnings start improving. Earnings should start improving soon as all the one off impacts of write-offs should be behind them or very nearly so.

I recently read an interesting perspective on current market structure from Kevin Muir of the Market Huddle, reprinted with permission by Kuppy of Praetorian capital. In it you will find what I believe is the correct answer as to why the short interest in MPW is increasing, despite fundamental improvements.

https://pracap.com/whats-driving-stocks/

Since all that matters to the quantitative strategies today is improved earnings, it is interesting that rents on the restructured hospitals will be starting in Q1 2025, and escalating for two years to reach their full amount in Q4 2026. That will provide artificial earnings growth for MPW, aside from whatever organic growth that management can provide. I had not initially planned on holding MPW for that long, I sorely desire to recycle these funds quickly to other opportunities, and I will sell some on any decent short squeeze, which should come from the first quarters of sequential GAAP earnings improvement.

Keep in mind, the negative earnings is due to writedowns, and when those are finished, EPS should be between $0.16 and $0.22 per quarter, meanwhile forecasted estimates are for earnings of $0.02 to $0.04 per quarter. When the write-offs are done, the earnings beats will be huge. MPW has $1.2 billion of debt maturing in 2025, and their creditworthiness is still suffering under the short attack, so management did guide to potentially a few more asset sales to continue deleveraging with maybe a partial refinance if they can get a good rate.

FTC Solar (FTCI)

In this last quarter, FTCI announced three new major contracts, 500 MW on Sept 10th, 1 GW on Oct 23rd, and 1 GW on Nov 4th. The consequences of this new backlog are that the stock price has fallen from about $0.51 when I did the writeup to $0.40 now. It is counter narrative, allegedly Trump will be bad for solar. But I maintain that the already allocated funds will still be spent, blue states won’t slow down, and hydrocarbon poor countries might have a genuine use case for solar. Narratives are important, and might keep FTCI’s price depressed, but this new CEO is full of hustle.

The major challenge for FTCI was that they were the market leader in a type of tracker hardware that lost market share, and had no presence in the market for the type of tracker hardware that customers preferred. Instead of solar panels having an individual dual-axis tracker, the marketplace discovered it was cheaper and more efficient for solar panels to be attached to the same tube that only moved on one axis. FTCI has transformed from having 15% of revenue on these tube tackers to 70% of revenue from this dominant technology. This is a major transformation of the company, and it was successful.

On the negative side, FTCI needed cash in order to bridge the gap to fulfill their project backlog. They raised $15 million in debt at 11% interest, and gave away warrants equivalent to about 14% dilution. This is obviously bitter-sweet news, but FTCI has a much more clear path forward, and is in a much less risky position moving forward. They still are not yet at a scale to cover fixed costs, but management believes they will flip to profitability within 2025.

Nerdy (NRDY)

An overlooked Trump platform beneficiary, it is now being recognized that the new administration might aggressively shift federal funding away from physical universities and toward online tutoring. Nerdy could be a major beneficiary of this, as would Coursera (COUR). If you would like me to prioritize a deep dive into Coursera, please let me know in the comments. Also, the Founder and CEO of Nerdy just made another large insider purchase, increasing his ownership stake in the company further. Since July, his ownership stake has increased from 20% of the company to 41% of the company. While this is an incredible vote of confidence, it also raises the risk of him attempting to take Nerdy private. How liquid are these markets that someone can accumulate 21% of a company without moving the price? Perhaps too liquid. On Tuesday, NRDY’s stock price went up 26% from $1 to $1.26. This small amount of momentum and narrative shift could ignite an enormous rally for this stock, I plan to buy some at the open tomorrow.

Operationally, NRDY experienced some growing pains in their integration with K-12 school systems this quarter. But, the CEO is a tech founder, and he is iterating, making changes, and sounds confident in his ability to meet the challenges and capture the opportunity ahead. The business plan still seems plausible to me. Management is guiding toward a significant increase in EBITDA next quarter, and for momentum to continue into 2025, but NRDY will still be operating at a loss for at least one more quarter. Cash on hand is around $65 million, there is no debt, and next quarter’s loss is projected to be around $4 million and shrinking, so there is plenty of runway for volume to overtake their fixed costs.

Keep reading with a 7-day free trial

Subscribe to Value Degen’s Substack to keep reading this post and get 7 days of free access to the full post archives.