1500 subscriber milestone special; The Container Store (Reprise) $TCS

Nothing but Gratitude

Thank you to all of you who have subscribed to this Substack. It has been quite a journey since starting on May 26th, and I am humbled that I can pay my half of the mortgage writing about businesses that I want to analyze for my portfolio. Every retweet and every restack goes a very long way toward helping me reach a bigger audience, and I am grateful for all of them.

I am a bit overwhelmed when I dive into the statistics that Substack provides. In the last few days, when I write an article, it is read by about 2,000 people. That’s more than the population of the small town in Maine where I am originally from. People are reading my writeups in 77 countries, including Kazakhstan, Denmark, New Zealand, and South Korea. The world might be becoming a very small place, but I remember when the only glimpses of faraway lands were found in National Geographic magazines in the school library.

But enough waxing nostalgic, I wanted to write today about the same company I wrote about for the 100 subscriber milestone special, The Container Store (TCS).

100 subscriber milestone special; The Container Store $TCS

Thank you to my first 100 subscribers, and a special thanks to Tommy Deepwater who in retweeting my third ever article on Transocean (RIG), got my tweet seen by 15,000 eyeballs. Another special thanks to the ROI Channel who restacked my article on Vertex Energy (VTNR).

There was a bit of drama for The Container Store recently, a relatively unknown investor suddenly acquired an 18% stake in TCS. The stock price has been giving observers whiplash ever since.

In response to this sudden 18% stake from a new investor, management immediately enacted a poison pill that expires in October of 2025 to prevent this new investor from increasing their stake or pursuing an activist strategy.

It turned out that this poison pill measure probably wasn’t entirely necessary, the sudden large position came from Amit Agarwal, a former patent attorney who lives in St. Petersburg, Florida. Amit believes in taking large positions and swinging for the fences, but he has not engaged in activism in the past.

Amit told a Bloomberg reporter, “there’s a gem inside this pile of mess and it will shine brightly enough to capture a buyer’s attention,” but “I could be wrong.”

TCS being taken private or being acquired is not my preference. When something is deeply undervalued, I don’t want a quick 20% bump in the stock price, I want it to grind higher into a multibagger. I believe that Leonard Green & Partners, the 30% owner and private equity firm feels similarly. There is no need to cut the gains short on this investment.

There is another LP with a large ownership stake in TCS, Glendon Capital, who owns 9.2%. An interesting twist is that Glendon Capital is primarily focused on distressed credit. For a distressed credit fund to do their due diligence on a company’s bonds and turn around and say, “No thanks, we prefer the common equity over the CCC+ ranked debt,” is a pretty powerful statement. It bolsters my confidence that my original analysis on the brand and their position is correct.

The majority of TCS’ liabilities are leases on their retail locations, and the intimidating weight of the full liabilities is just a regular rent payment as long as TCS is a going concern. There is some question about TCS’ ability to refinance their debt, especially a term loan which matures in 2026. While the debt maturity wall is a concern, JP Morgan just extended a revolving credit facility at SOFR +1.25%, which is a very attractive rate. This would indicate that TCS should have no problem refinancing their long term debt if needed.

I have little doubt the stock price would improve in the short run if management focused on paying down debt instead of opening new stores. But so far management has been focusing on their growth strategy, plowing depreciation into new store openings. This may prove to generate the higher returns eventually, if TCS stays public long enough to enjoy it.

While business is currently in the doldrums for TCS, this is almost certainly due to temporary cyclical factors, and is not likely an indication of a structural decline of the business. 2022 EBITDA was $159 million, or about 8x trailing twelve month interest expense. Last quarter was particularly disheartening, but seasonally, Q2 has always been their weakest quarter, and management indicated that they are witnessing an improvement month over month. There are good odds that Q3 results should show some incremental improvement quarter over quarter due to seasonality, even if the current consumer durables slump leaves TCS down year over year.

If you look past the $101 million goodwill writedown, trade name impairment, and other unusual items in the last twelve months, from a cash perspective, TCS is still a melting ice cube, but melting very very slowly. A trailing twelve month loss of $7 million is a lot more tolerable than a trailing twelve month loss of $108 million. Given this slowly deteriorating situation, the biggest question then is how long will it be until cyclical headwinds turn into tailwinds. This can be broken down into two trends, the K-shaped economy, and the frozen housing market.

The K-shaped economy theme is still playing out. More and more data points come along demonstrating that the upper class is still spending and still doing fine, fueled by their 4.5%+ money market income and a stock market at all time highs. Meanwhile, at the lower end of society, mass immigration has driven up rents and driven down wages, creating an immiseration that is fueling a populist backlash. Purchasing power of the lower classes is completely flat in the post-Covid period. The K-shaped economy thesis is still relevant, and is likely the reason why, excluding unusual items, TCS would have had 2022 EBITDA of $159 million and 2023 EBITDA of $111 million, despite rising interest rates. It is only in this most recent consumer armageddon that TCS is really in a pinch.

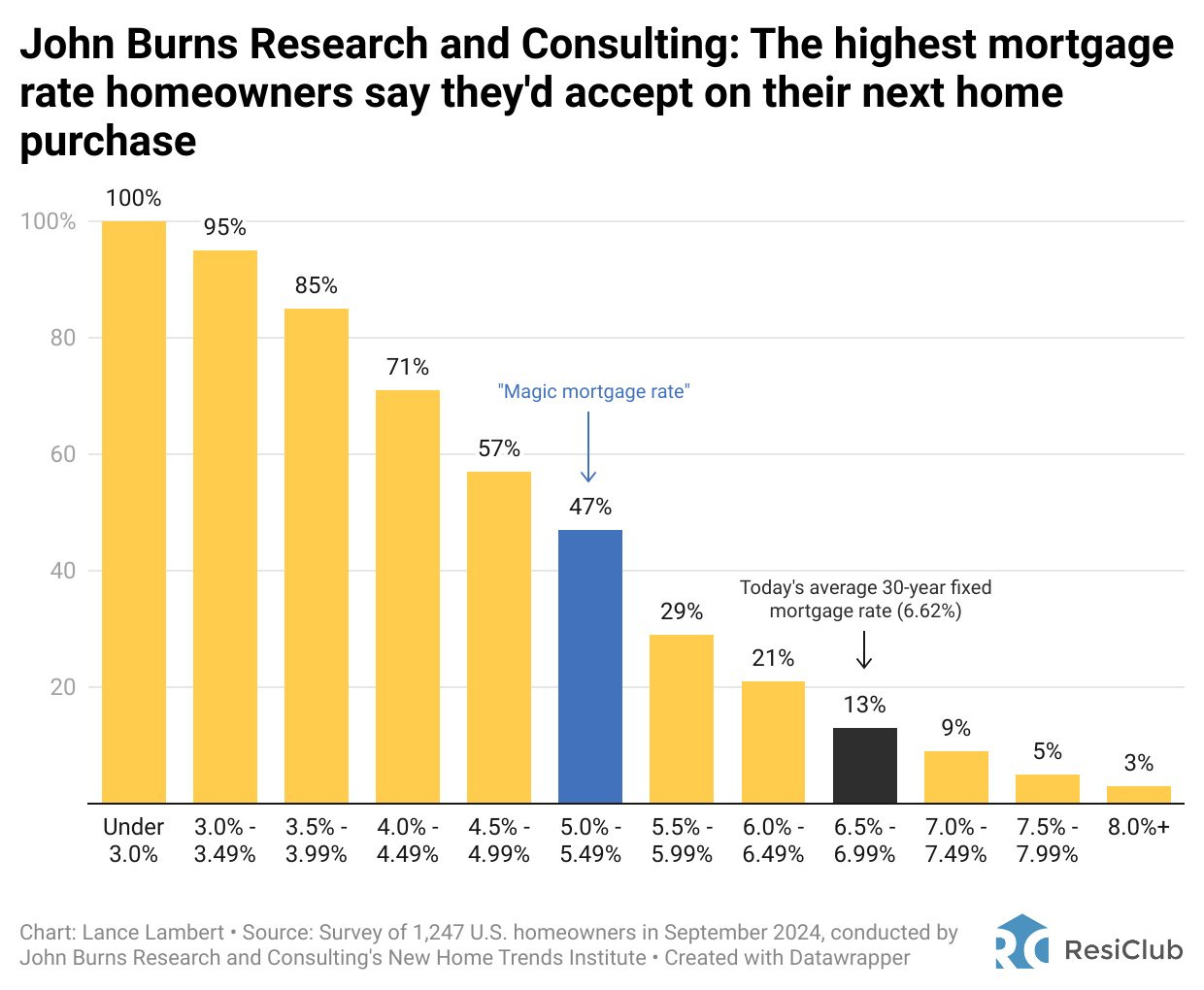

But the existing housing market is still frozen, and TCS will have a hard time growing their custom closet business without housing turnover. In surveys, consumers have indicated that a mortgage rate of 5.5% is just about their reservation threshold for buying a new home. As I write this, 30 year fixed conforming mortgage rates are 6.5%. The 10-year treasury is just a bit under 4.1%, resulting in a 2.4% spread between mortgages and treasuries. The mortgage spread average is closer to 1.5% to 1.7%. This means that even at current treasury rates, mortgage rates could come down to meet the reservation threshold of consumers, if the spread narrowed.

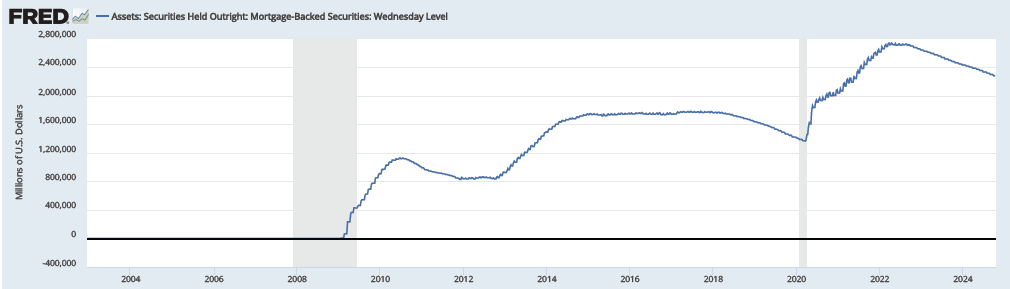

I believe the likely cause of the wide mortgage spread is the Federal Reserve’s quantitative tightening, letting mortgage backed securities mature and not replacing them. MBS on the Fed’s balance sheet has dropped from $2.7 trillion to about $2.2 trillion since Jerome Powell embarked on his tightening journey. Unfortunately, with employment data coming in strong, and inflation data coming in hot, it is not apparent when or if Jerome Powell would embark on quantitative easing again. And even if he did, with a government fiscal deficit of 6% to 7% of GDP, even if the Fed did engage in a new round of quantitative easing, it might be forced to focus on treasuries alone, ignoring mortgage backed securities all together.

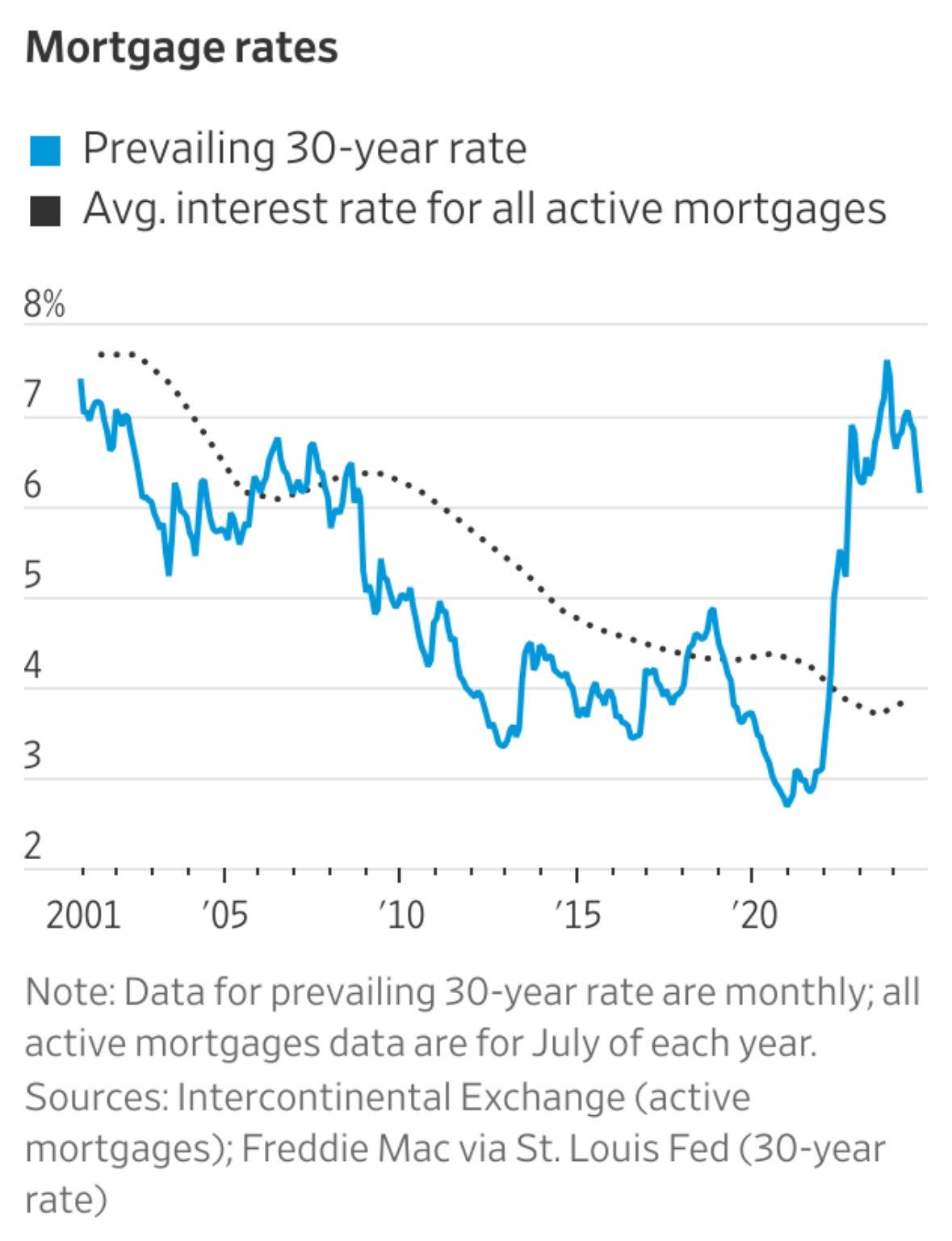

This would mean that the 30 year mortgage rate is not likely to meet consumer’s 5.5% mortgage reservation bid, and it will have to be the consumer who changes their expectations rather than the mortgage rates which will change. How long will it take for consumers to be content with 6.5% mortgages? That could be a year or two. You can see in the graph below that so many homeowners refinanced at cheap rates during the low interest rate period, and the housing market has been so frozen, that even with mortgage rates high for the last two years, the average existing mortgage is still below 4%.

It might be more likely that housing prices could stay flat, or maybe even fall by some modest amount in 2025 as inventories are on track to return to pre-Covid levels sometime in 2025 or 2026.

My best guess is that homebuyer expectations are going to slowly adjust to 6.5% mortgages, and home prices will stay somewhat flattish, allowing the existing home sales market to slowly thaw out, and giving the durable goods market some sort of reprieve within the next 12-18 months. This should give The Container Store some small tailwind to bolster their custom closet business, which even in their worst quarter since Covid, still grew at 1.9% while their general merchandise business shrunk by 20% year over year.

I don’t think it will take much positive momentum to get TCS from a $50 million market capitalization to a $150 million market capitalization. The goodwill writedown rolling off the trailing twelve month metric, quarterly earnings that have positive quarter over quarter growth, positive operating income, debt refinancing, etc. These are all near term catalysts that could bring some more attention to the egregiously underpriced business.

In order to get TCS back toward a price to sales ratio of 1.0x, it will probably take at least a few years of growth and positive free cash flow. But from the current stock price, a return to 1.0x price to sales on a $1 billion revenue run rate would make TCS a twenty bagger, if the large shareholders are willing to stick with it and don’t take the company private beforehand.